At a glance

- Quality, affordable housing is out of reach for far too many Americans. This issue touches rural and urban households, young and old, poor and middle class, and households across racial groups.

- Housing, and where that housing is located, matters a lot. Housing significantly determines access to employment, education, public and social services, and critical amenities that help families achieve economic mobility.

- The housing crisis is a national issue, and it disproportionately burdens Black Americans. Nearly 60 percent of Black renters and 30 percent of Black homeowners are moderately or severely cost burdened, well above national averages. Legacies of housing discrimination are compounded by continued supply, demand, and geographic imbalances that create acute housing challenges for Black families and impede their pursuit of economic opportunity.

- A shortfall of housing underpins the current crisis. There were 8.2 million fewer housing units than needed in 2023 to meet the needs of American families. Without decisive action, that gap could grow to 9.6 million units by 2035.

- While not without trade-offs, investing to close this housing shortfall could unlock as many as 1.7 million jobs and add nearly $2 trillion to GDP through 2035. These gains would ripple across the US economy. Because Black Americans shoulder an outsize share of the housing burden, they would see material benefits.

- We highlight five housing themes, based on a deep analysis of more than 80 ideas. The themes are unlocking land through creative incentives and partnerships, augmenting programs to unleash private capital, scaling off-site home construction, reinvesting in public housing and shared-equity models, and revamping housing choice vouchers. Together, these actions could unlock an estimated 2.3 million housing units, including 700,000 for Black households, over the next decade.

Mapping the US affordable housing crisis

A data visualization presentation examining the scale of the housing challenge with county-level data.

Housing can be, and historically has been, a gateway to economic opportunity. However, it is increasingly an economic barrier for American families. There is broad recognition that the relentless increase in the cost of renting or owning a home in the United States has put many already vulnerable families at further risk, widening inequality.1

And as with other aspects of the US economy,2 Black Americans are particularly vulnerable. Rising prices and constrained supply have been most prevalent in megacities and other urban areas, where nearly 50 percent of Black families reside.3 Unaffordability is among the key reasons Black families are more likely to live in neighborhoods with challenged public schools4 and limited access to green spaces5 and other amenities that increase quality of life.6 Having a limited number of quality homes7 in mixed-income neighborhoods that are affordable8 also restricts job access, creating a drag on both workers and the broader economy.

At the same time, recent trends have intensified these challenges for all Americans. Consumer prices have risen at rates not seen in decades, leaving families, particularly those with less income, vulnerable and with less to spend on housing.9 For would-be homeowners, mortgage rates rose sharply on the back of higher inflation and interest rate increases. Constrained supply has kept home prices and rents from adjusting downward, leaving the ambition of owning a home or renting affordably out of reach for many Americans.

Ideas abound to address the crisis. Some have shown promise; others have not. Many solutions are local in nature and have yet to scale successfully to other regions. New technologies that have increased productivity and brought down the costs of other goods have yet to gain significant traction in housing.10 Plans for mixed-income and higher-density housing often run into local opposition. Financial innovations have yet to overcome credit constraints facing lower-income borrowers. The housing crisis has gotten worse.

This report aims to reimagine how housing could be a tool to accelerate economic mobility and produce widespread benefits for Black families and the United States (see sidebar “Defining economic mobility”).

In chapter 1, “The challenge of housing and economic mobility,” we examine the roots of the nationwide 8.2-million-unit housing shortage, which, absent forceful action, will likely climb even further (Exhibit 1). Our estimates go beyond most models by factoring in overcrowding—which we define as households with more than one occupant per room (excluding bathrooms and kitchens).11 This contributes 3.7 million housing units to our 9.6-million-unit gap estimates by 2035. Research suggests this is indicative of declining housing and living quality due to financial strain, especially for minority households.12 This national challenge affects many types of communities, and these signposts involve more than just numbers. They are barriers to opportunity for millions of Americans.

In chapter 2, “The opportunity,” we quantify the potential benefits to the US economy and American families of addressing the housing crisis and closing13 the undersupply gap by 2035. While not without trade-offs, doing so could add nearly $2 trillion to GDP through greater investment and economic activity in housing-related sectors (for example, construction) and related supply chains, and create nearly two million new jobs across sectors—gains that would materialize gradually over the next ten years.

For households, addressing housing supply issues could help reduce financial stress while cutting annual inflation in housing prices nearly in half (to 2.1 percent compared to 3.8 percent without intervention). In all, roughly six million cost-burdened households stand to benefit from addressing the housing gap. A range of US families, including Black households, would experience employment gains and greater financial stability.

We further spotlight three housing-challenged metro areas with significant Black populations: Atlanta, Chicago, and Washington, DC.

We recognize that addressing the housing crisis and closing these gaps is a complex and resource-intensive endeavor that could face numerous barriers, including resistance from industry actors and residents who may benefit from current market conditions. Overcoming these challenges will require creative approaches and proof points that help demonstrate the long-term value of this endeavor for a range of stakeholders and the broader economy.

In chapter 3, “Bold solutions for a promising future,” we highlight five key themes based on an analysis of more than 80 documented and researched approaches, along with dozens of expert interviews. These bold solutions are more relevant in some community profiles than others, but all could help advance economic mobility, particularly where housing could be unlocked in economically diverse neighborhoods with access to critical resources (such as transit, jobs, and quality schools). The five key themes are unlocking land through creative incentives and partnerships, augmenting programs to unleash private capital, scaling off-site home construction, reinvesting in public housing and shared-equity models, and revamping housing choice vouchers. We examine why, and where, these innovations have worked and how they might be reimagined and scaled throughout the country. We quantify the impact these innovations could have if they were deployed at scale.

After decades of study and analysis, one thing seems clear: There is no single solution that will solve the US housing crisis. But if many of the solutions outlined in this report were reimagined, tested, and scaled, they could significantly improve the housing experiences of millions of American families, particularly Black families.

Chapter 1: The challenge of housing and economic mobility

Housing is much more than the dwellings where people live. It serves as a core enabler of individual and family health and well-being, job opportunities, education, green spaces, and wealth. A home—whether rented or owned—is fundamental to one’s ability to achieve economic mobility.

Yet a home that is affordable, safe, and of good quality is increasingly out of reach for far too many Americans. This reality has few social or economic boundaries. It affects rural and urban households,14 young15 and old,16 poor and middle class17—across racial groups. Nearly 70 percent of Americans are concerned about the rising cost of housing, an increase of eight percentage points from 2023 to 2024.18

More older adults than ever are cost burdened,19 with 11.2 million individuals over 65 spending upward of 30 percent of their income on housing.20 At the same time, homeownership among young adults has declined since 1990, reflecting the pervasiveness of housing challenges.21

As of 2023, the United States had 8.2 million fewer housing units than required to meet the needs of American families, driven by mismatches in supply and demand as well as by geographic imbalances. Without decisive action, this gap could grow to 9.6 million by 2035.

This undersupply has far-reaching consequences, including escalating costs and financial insecurity. From 2019 to 2023, a period that included the COVID-19 pandemic, the gap between housing costs and household incomes widened, with rents rising 30 percent compared with a 20 percent increase in wages—highlighting the mounting strain on households.22

Persistent supply-and-demand imbalances have made affordable, quality housing increasingly unattainable. These barriers limit opportunities to rent or own and exacerbate long-standing economic inequities.23

Specifically, housing influences economic mobility in four critical ways,24 all of which are particularly relevant to Black Americans.25

- Housing dominates family budgets. Housing is the largest single expenditure for most households, typically more than double transportation or food. Households are considered cost burdened if they spend 30 percent of income on housing. In 2022, one-third of US households were considered severely or moderately cost burdened,26 while 47 percent of Black households were in that category.27

- Neighborhoods shape opportunity. Access to jobs, schools, services, and amenities is heavily influenced by housing. A reliable place to live enables people to go to work, attend school, and participate in their communities. Research shows that every year spent in a higher-quality neighborhood increases a child’s earnings in adulthood.28

- Jobs: Geographic proximity affects employment,29 hours worked, wages, and transportation costs. In many areas, investment in public transportation infrastructure still occurs disproportionately in counties where Black households are underrepresented.30

- Schools: Where families live often determines which public schools their children can attend. Research31 shows that better school quality in a zip code correlates with higher home prices. This relationship is particularly strong in metro regions with greater income inequality. One in five Black residents lives in a high-poverty neighborhood (even if they themselves are not experiencing poverty), compared with one in 25 White Americans.32

- Neighborhood amenities: Location influences access to parks and restaurants, healthcare, grocery stores, and other essential services. Compared with White Americans, Black Americans are 2.4 times more likely to live in a healthcare desert.33 Communities that are predominantly Black are more likely to be food deserts—that is, areas that lack grocery stores or other places to buy fresh, healthy foods.34

-

Housing is key to physical well-being and safety. Substandard housing disproportionately affects low-income households, exposing them to health and safety risks such as lead, mold, and structural deficiencies that contribute to chronic health issues. Black households are particularly vulnerable, with a greater likelihood of residing in inadequate housing relative to other racial or ethnic groups (Exhibit 2).

For example, a report from the Urban Institute35 highlights that nearly three-quarters of housing complaints related to chronic health concerns and safety hazards in Philadelphia came from areas with higher-than-average poverty rates. More than two-thirds were in areas with an above-average share of Black residents. Black Americans are nearly one-third more likely than White Americans to perceive their neighborhood as having a significant impact on their health.36

- Homeownership remains a driver of wealth. Home equity is the largest financial asset for most middle-income families, representing between 50 percent and 70 percent of net wealth.37 For many Americans, homeownership remains a reliable path to wealth accumulation38 and is a key driver of the racial wealth gap.39 The Black–White homeownership gap widened from nearly 24 percentage points in 1970 to more than 29 percentage points in 2022 (Exhibit 3).40 Black households are less likely to own than White households at every income level. Inequitable lending practices continue to limit asset-accretive homeownership opportunities for Black Americans, with cascading effects (see sidebar “A legacy of discrimination”).

The affordability crisis disproportionately burdens Black Americans

One of the core challenges of the housing crisis is a shortage of housing units. This shortage is driven by three key factors: high land and construction costs, scarce capital for affordable housing, and limited incomes and support for families (Exhibit 4).

These factors create outsize challenges for Black Americans for two key reasons: 1) Black Americans are more likely to live in communities where housing supply is particularly limited relative to demand, and 2) they are disproportionately represented in the lowest income quintiles, where housing challenges are most prominent (see sidebar “Community profiles”).

Black Americans are overrepresented in communities with housing shortages

Single-family zoning—which applies to 75 percent of US residential land41—and complex building restrictions have combined to constrain supply across the country, particularly in urban areas with robust economies and strong job prospects (Exhibit 5).

Megacities account for 25 percent of the housing gap, equaling about two million units, followed by the urban periphery. This supply shortage disproportionately affects the nearly one-third of Black Americans in megacities such as New York City, San Francisco, and Atlanta (Exhibit 6). Black households in these communities are moderately and severely cost burdened at higher rates than in other areas, even at higher income levels.

Localized shortages affect affordability

Housing undersupply has an acute impact on both home prices (Exhibit 7) and rental markets, where costs have grown steadily over the past decade. Between 2012 and 2023, megacities saw annual home price increases of 7.3 percent, above the national average growth rate of 6.8 percent. These increases placed a financial burden on households—particularly Black and low-income families.

Rental markets have experienced similar pressures. Areas such as Dallas County, Texas, and Fulton County, Georgia, saw rent increases of more than 5 percent annually between 2015 and 2023, versus the national average of 4 percent.

Despite growing demand, the total number of housing units with monthly rents below $600 has declined. Nationwide, the number of low-rent units,42 adjusted for inflation, fell from 8.3 million in 2012 to 7.2 million in 2022.43

Housing unaffordability and lack of savings were the two most cited barriers to homeownership. Similarly, cost of living is the top reason for voluntary moves among Black Americans, according to our survey of thousands of households conducted in summer 2024.

Addressing these entrenched challenges is a necessity—and an opportunity to create widespread economic and social benefits.

Black Americans are disproportionately represented in the lowest-income quintile, where housing affordability challenges are most prominent

More than 70 percent of households in the bottom income quintile (annual household income under $40,000) are severely or moderately housing cost burdened, including nearly 92 percent of renters and 63 percent of homeowners.44

- Nearly 55 percent of households in the bottom income quintile are severely cost burdened, meaning they spend more than half of their income on housing costs. Eighteen percent are moderately cost burdened, spending 30 percent to 50 percent of income on owning or renting a home.

- In the second quintile—household income from $40,000 to $71,300—47 percent of households are severely or moderately housing cost burdened; 20 percent are severely housing cost burdened, and 27 percent are moderately burdened (Exhibit 8).

The affordability challenge is even more apparent for Black families; more than one-third are severely cost burdened across all income levels, the highest of any demographic.

The affordability challenge for Black households is particularly pronounced in the South, where more than half of Black Americans in the bottom 40 percent of income reside, and which accounts for a majority of severely cost-burdened Black households (Exhibit 9).

Chapter 2: The opportunity

In the previous chapter, we established housing as a cornerstone of economic mobility and laid out the urgency of addressing the projected 9.6-million-unit housing shortfall by 2035. In this chapter, we explore the broader opportunity: How can bridging the gap unlock sustainable, inclusive economic growth?

To answer this question, we explore the transformative ripple effects of targeted investments in housing. At its core, the crisis affects the entire economy. Constrained housing supply can serve as a major barrier to economic growth; one study suggests that a lack of housing may have lowered aggregate US GDP growth by up to 36 percent between 1964 and 2009.45

A constrained housing market creates a “spatial misallocation” of talent and resources.46 The result is limited individual geographic mobility and muted aggregate productivity, limiting the nation’s economic potential.

Targeted housing investments could unlock benefits in four critical areas: GDP growth, job creation, increased tax revenues, and improved housing affordability. The impact could also drive increased productivity, labor mobility, and wealth creation—key ingredients for inclusive and sustainable growth. For example, just as other sectors are harnessing artificial intelligence to transform their businesses,47 housing could increasingly leverage AI and other emerging technologies to reduce construction costs and improve the quality of manufactured homes, for example, and improve the delivery of housing-related financial services. Technology could be a key enabler to unlocking these opportunities.

Closing the affordable housing shortfall would do more than address inequities. It could offer national opportunities to fuel economic growth for households and communities and across industries.

Because Black families have suffered disproportionately from the housing shortage, our impact model suggests they would experience many of the benefits of addressing the crisis—14 percent of all households lifted out of cost burden are Black, despite representing only 12 percent of overall households. That said, Americans of all races and ethnicities would experience significant gains, both directly and indirectly, from a less supply-constrained housing market.

At the same time, we recognize that capturing this opportunity would require trade-offs. Given tight labor markets, labor shortages in construction trades,48 and the importance of other critical national investments (such as education and healthcare), the task at hand would not be easy. That said, if the public and private sectors in the United States could create the capacity and investment needed, the benefits of closing the housing shortage could be meaningful.

National impact: Economic growth and jobs

Macrolevel implications:

- Housing investments have a multiplier effect on economic growth and tax revenues. Closing the gap by 2035 would mean building 9.6 million housing units on top of the roughly 850,000 units per year already expected from 2023 to 2035. This incremental investment could generate nearly $2 trillion in cumulative GDP gains throughout the construction supply chain, equivalent to Brazil’s 2023 economic output. This growth would be fueled by an estimated $2.7 trillion in cumulative investments (Exhibit 10).

- Second-order effects49 could add even more,50 driven by additional job creation, earnings, and consumer spending tied to expanded construction activity.

- Addressing shortages could enhance labor mobility. Assuming housing production increases from 843,000 to 1.7 million units per year, it could add nearly two million new jobs, including more than 700,000 in construction trades.51 For Black Americans—who represent only 5 percent of employment in construction trades—an estimated 55,000 new jobs would be created, increasing household income of these workers by $40,000 on average. Asian workers similarly represent a small share of construction workers and could take on roughly 10,000 new jobs. The difference is even more significant for Latino workers, who could gain an estimated 280,000 new jobs. White workers, who account for more than half of the industry, could stand to gain 370,000 jobs.52

- Housing investments—and subsequent economic uplift—may help alleviate housing-related cost pressures. For example, we estimate the median US household income may grow 3.2 percent annually from 2022 to 2035. Additionally, by building housing required to meet the 9.6-million-unit housing supply gap, we estimate home prices may grow at 2.1 percent per annum (below expected household income), alleviating cost pressures. Conversely, if the housing supply gap is not addressed, supply tightness may push prices to grow by 3.8 percent annually (above expected household income growth), worsening cost pressures.

- Lower- and middle-income families—including a significant portion of Black Americans—stand to benefit as more jobs become available, incomes increase, and housing becomes more accessible and affordable. Overall, the number of cost-burdened households could decrease by around 15 percent.53

- Across races, nearly six million cost-burdened households stand to benefit from addressing the housing gap, by no longer being cost burdened.

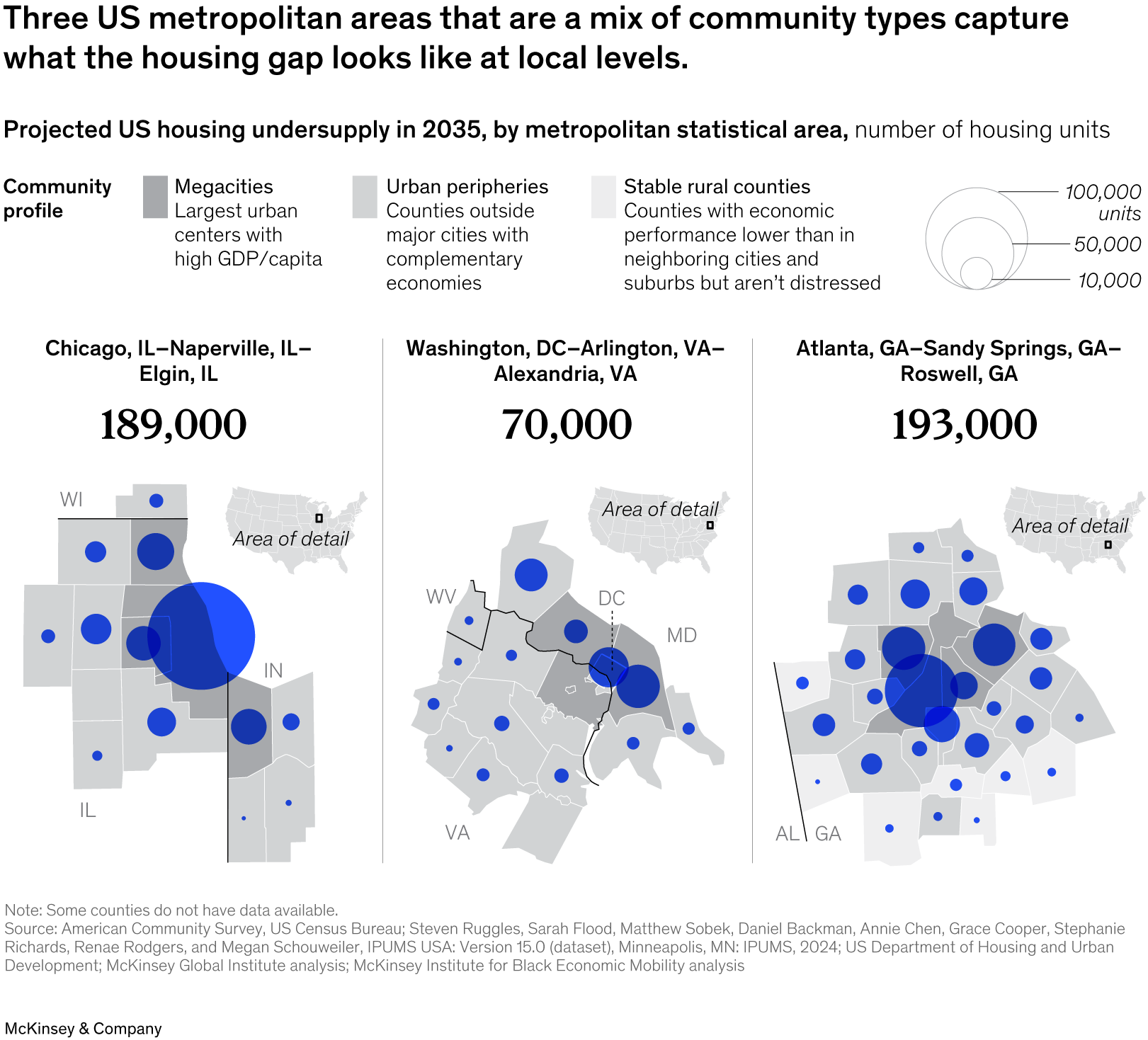

Community impact: Spotlight on Atlanta, Chicago, and Washington, DC

While our research is national in scope, metro areas such as Atlanta, Chicago, and Washington, DC, help provide compelling examples of the localized economic potential of greater housing investments. These cities are highlighted as examples given their geographic diversity, their significant Black populations, and the scale of the housing challenges they face. Estimates for housing units were developed using the same methodology as our national model, while investment and impact accounted for each city’s unique demographic composition and housing costs. These cities represent three common community profiles—megacities, urban periphery, and rural cities—which together account for more than 50 percent of the nation’s housing shortage (Exhibit 11).

- Chicago: Addressing the 189,000-unit shortfall (in excess of expected housing construction) would require $54 billion in investment, contributing more than $30 billion to the local economy and generating nearly 27,000 jobs by 2035. Following through on this investment may lower the total number of cost-burdened households by 13 percent (about 200,000 total).

- Washington, DC: Closing the 70,000-unit gap54 would require $22 billion in investment, generating an additional $11 billion in economic growth and creating nearly 10,000 new jobs by 2035. If this is addressed, 10 percent of cost-burdened households may experience relief (about 70,000 total).

- Atlanta: Bridging the projected 193,000-unit55 housing gap would require $63 billion in investment. This could drive $36 billion in economic growth and create more than 34,000 jobs. Lower housing costs may decrease the number of cost-burdened households in the city by more than 20 percent (about 150,000 total).

Chapter 3: Bold solutions for a promising future

The previous two chapters outlined the dramatic scale of the housing crisis and highlighted the significant benefits that resolving it could offer households, communities, and the economy.

This crisis is unlikely to be resolved with a one-size-fits-all approach. Rather, targeted solutions tailored to local and regional challenges, executed collaboratively by many different stakeholders, offer the most promise.

In the private sector, developers, development corporations, financial institutions, insurers, investors, and manufacturers play crucial roles in construction and housing finance. The public sector—encompassing federal, state, and local governments, along with public housing authorities (PHAs)—is critical for funding and subsidizing housing (particularly for the most financially vulnerable), creating innovative incentives to leverage private capital effectively, enforcing zoning and land use policies, and managing public programs. The social sector, including philanthropy and nonprofit providers, is key to supporting novel solutions and risk-taking, advocating for families, and supporting effective direct services and supports.

Understanding and leveraging the distinct roles of these stakeholders can help our nation collectively address the challenges of affordable housing.

Our research aims to build on the extensive work of institutions and individuals who have been pursuing this work for generations. Different strategies have shown varying levels of success, but even what “works” is happening in piecemeal ways in pockets of the country—and many well-intentioned solutions face significant implementation challenges on the ground.

This chapter shines a light on a handful of potential solutions that have been shown to work (or have the potential to do so), aims to uncover what barriers often impede these solutions from scaling, and explores creative approaches to a path forward.

Our approach

We conducted a meta-analysis of research published in the past decade by more than 50 think tanks, academics, industry associations, nonprofits, and others to catalog a list of over 80 solutions to explore (see appendix, section 2 for the full list of solutions). We then shortlisted these solutions based on four factors:

- Relevance to Black residents. A solution is more likely relevant if it focuses on places where Black Americans are concentrated or if it addresses specific barriers Black residents face.

- Strength of evidence. There is robust evidence demonstrating the solution’s effectiveness or emerging consensus based on early evidence or analogs.

- Potential impact. A solution has the potential to truly move the needle by significantly increasing supply or improving affordability.

- Feasibility. A solution may garner buy-in across stakeholders including government, residents, financial institutions, developers, and others.

We then conducted nearly two dozen calls with experts across the public, social, and private sectors. Ultimately, five themes emerged:

Theme 1: Unlock land through creative incentives and partnerships

The problem today

Zoning determines what housing is built where. Zoning restrictions limit where people can live—and have historically been used as a tool to prevent families, particularly Black families and those from other racial and ethnic groups, from living in certain communities.56 Zoning restrictions can also increase housing prices by limiting supply.

Higher-density development appears central to addressing the affordable housing crisis. Within a 15-year window, around 150 policies have taken shape across nearly 100 municipalities in pursuit of zoning changes.57 These include reducing minimum lot sizes, changing parking requirements, and expanding multifamily zoning.

While many experts, advocates, and policymakers agree that zoning reforms are critical, many of these well-intentioned changes are limited in scale, speed, and efficacy. Governments may be wary of backlash from vocal opponents and pushback from residents. Jurisdictions often lack the capabilities and know-how to optimize vacant land—which, by some estimates, accounts for 17 percent of urban land in the United States.58

To address these impediments, we outline three strategies inspired by innovations inside and outside the United States.

Example 1: Leverage transit to provide incentives for improved zoning

States can provide incentives for communities to fund higher-density development near public infrastructure. While state initiatives may aim to enhance affordable housing options, they may also inadvertently cause displacement. Therefore, it is critical to adopt measures to ensure existing residents are not forced out of their neighborhoods.59

- Colorado’s 2024 Housing in Transit-Oriented Communities law (HB 24-1313) requires 31 municipalities to build higher-density residential development, of at least 40 units per acre, within a quarter mile of bus stops and a half mile of rail stations. The law includes a $35 million competitive grant program, which awards infrastructure funding to communities to upgrade transit and neighborhood centers. Other jurisdictions could explore similar competitive programs.60

- As part of a 2021 Economic Development Bill, Massachusetts passed legislation similar to Colorado’s, requiring 171 rapid transit communities to enact rules that zone at least one district for multifamily development “by right” (instead of by discretionary review process).61 Unlike Colorado, Massachusetts established penalties for noncompliance. Communities with rapid transit facilities that fail to enact required zoning reform may lose funding eligibility for other programs. Massachusetts’s transit-oriented legislation, Chapter 40A of the state’s Zoning Act, has been particularly effective at increasing housing supply because it complements prior legislation allowing developers to appeal aspects of zoning laws that limit building height. Other communities might look to couple transit infrastructure funding with housing development in similar ways.

Example 2: Increase incentives for existing residents via direct financial benefits

While states can help local jurisdictions circumvent some challenges in reimagining land use, many may still encounter opposition from residents. Studies have demonstrated that affordable housing development is not correlated with trends in crime, property values, or taxes.62 This section focuses on incentives; however, we acknowledge that opposition to land use may be unmerited.

In Massachusetts, 54 percent of voters in Milton—a predominantly high-income, owner-occupied suburb—rejected proposed zoning reforms even at the expense of losing funding for public projects, including a $140,800 grant for seawall improvements.63 A more novel solution could provide incentives to existing residents more directly via direct financial benefits:

- Some state and local governments use tax increment financing (TIF) to fund development projects through future property tax increases.64 The process starts with the establishment of baseline revenues based on current property values within the municipality. Over time, as private or public development drives up value, the incremental tax revenue is reinvested in infrastructure and other projects. Evidence on TIF is mixed. Some cities have successfully used it to establish dedicated revenue streams. For example, Portland, Oregon, sets aside 45 percent of TIF revenue for housing, which has generated roughly $83 million to support construction of 2,200 units of affordable housing.65 That said, critics have argued that this policy diverts revenues—which would have been captured even without the TIF-funded investments—away from other services, such as other public infrastructure.66 Some jurisdictions in California have begun innovating on TIF models, successfully forming enhanced infrastructure financing districts (EIFDs). EIFDs similarly capture incremental tax revenues but also empower local communities to determine how and where those revenues are used via community-empowered governance structures.67

- One approach could be to redistribute incremental tax revenues from rezoning directly to households. Through direct dividends, residents could gain a financial benefit from higher-density, mixed-income development. Taking inspiration from TIF and other direct-benefit incentive programs—such as the Alaska Permanent Fund (APF), a state program that distributes annual dividends to eligible residents from oil revenues generated by the Trans-Alaska Pipeline System—this approach might help reduce resident resistance to zoning changes. While learning and testing would be critical, this approach could help unlock housing in historically more resistant communities.

Example 3: Leverage public-private partnerships

Municipalities could accelerate housing development by more creatively leveraging public–private partnerships (see sidebar “Case study: Minneapolis”):

-

The Copenhagen (CPH) City & Port Development Corporation, established in 2007 as a merger of the Ørestad Development Corporation and the Port of Copenhagen, is a publicly owned, privately run corporation that manages publicly owned assets, assesses market value, and captures profits for public investment.68 National and local governments transfer underused assets to CPH City & Port Development, which rezones them for residential and commercial use. As the value of rezoned land rises, CPH City & Port Development secures low-cost loans from Denmark’s National Bank, enabled by Copenhagen’s AAA credit rating. The capital raised is used to invest in public transit, roads, and other urban amenities that improve the livability and attractiveness of the residential and commercial assets, and is reinvested to help service the debt.

Similarly, the Port of Greater Cincinnati Development Authority (the Port), established in 2001, has supported a range of cross-stakeholder investments intended to accelerate residential development. For example, in 2022, the Port purchased 194 single-family homes with the goal of renovating them and creating opportunities for affordable homeownership. Through the support of local government and philanthropy—as well as close collaborations with small minority- and women-owned contractor businesses and diverse real estate brokerage firms—the first slate of 19 homes has begun to have an impact on residents and local businesses.69

- The Denver Regional Transit-Oriented Development (TOD) Fund—a partnership of state and local housing agencies, philanthropic institutions, community development financial institutions (CDFIs), and major banks—promotes affordable housing alongside Denver’s transit expansions. The fund provides low-cost loans to developers, subsidizing land costs around transit centers. Between 2010 and 2022, the fund invested $50 million into 22 properties resulting in more than 2,000 new or preserved affordable units—double its goal.70

Impact of scaling these strategies

We estimate that if localities upzoned such that 3 to 4 percent of projected single-family housing starts are replaced with multifamily units each year for the next decade, the United States could add approximately 530,000 to 620,000 housing units and have an impact on 120,000 to 140,000 Black households from 2025 to 2034.71

If roughly one in five localities rezoned 5 to 6 percent of vacant public land for higher-density residential development, we estimate that the United States could add 490,000 to 620,000 units and have an impact on 70,000 to 140,000 Black households over ten years.72

Theme 2: Augment programs to unleash private capital

The problem today

Without subsidies and creative financing, it is often difficult for the investment underwriting for affordable housing to pencil out. Financing shortages are particularly acute for Black-led affordable housing developers, who frequently cite challenges in accessing capital.73

One solution that has helped make this work is the Low-Income Housing Tax Credit (LIHTC) program. A public-private partnership that leverages federal tax dollars to provide incentives for private investment, LIHTC is the largest source of new-construction funds for affordable housing development.74 Although it is not without its challenges, the program has financed the construction or rehabilitation of nearly four million units, contributed $257 billion in tax revenue, and generated more than $700 billion in wages and business income since 1986.75 From 2000 to 2019, LIHTC provided at least partial financing for 25 percent of new apartments built nationwide, according to the Urban Institute.76

But constrained financing and complex application processes limit the program’s efficacy and increase costs for developers, despite general support for the program. Most banks lack incentives—particularly without LIHTC financing—to underwrite affordable housing investments. Additionally, studies show that LIHTC projects are seldom placed in high-opportunity areas. To address this, states could consider revising their allocation strategies for LIHTCs to emphasize placement in neighborhoods that offer greater opportunities for residents.77

We examine four potential innovations that could further enhance LIHTC and help unleash other sources of private capital.

Example 1: Streamline LIHTC applications at the state level

Streamlining applications and centralizing funding sources may help fast-track affordable housing proposals and reduce costs for developers.

- One tax credit syndicator estimates that LIHTC arrangements with five or more soft funding sources add several hundred thousand dollars in administrative costs, while another estimates an extra 10 percent of total project costs.78 In California, each additional soft source for new LIHTC construction increases per-unit costs by roughly $6,500 on average, or 1.7 percent of per-unit costs.

- Pennsylvania offers a one-stop-shop model to help reduce costs.79 The Pennsylvania Housing Finance Agency (PHFA) consolidates numerous funding streams, including LIHTC, HOME allocations, and National Housing Trust Fund dollars, into one process—aligning LIHTC with other state and local funding. This allows the PHFA to automatically consider developers for multiple funding sources that have identical legal terms, similar requirements, and standardized monitoring processes. The PHFA handles all applications in-house with staff who are familiar with program requirements. This one-stop-shop approach could be a model for others to reduce the administrative burden (and related costs) of LIHTC processes.

Example 2: Consider refinements to the cap on tax-exempt bonds

In 2023, one in three states maxed out automatic LIHTC credits after reaching the private activity bond (PAB) cap. PABs are government-issued, tax-exempt bonds for private projects that serve a public purpose.

- When at least 50 percent of a housing project’s financing consists of PABs, it automatically qualifies for 4 percent tax credits. These credits subsidize 30 percent of low-income unit costs in a project. However, the federal government caps the number of PABs any state can issue each year based on a population formula.80

- Volume caps do not apply to critical infrastructure and other public services considered to be public necessities. Affordable housing could be viewed similarly and therefore also be considered exempt—with alternative sources of income identified to support the expansion of the cap.81

- State-level LIHTC programs could provide a model to better inform federal action. Colorado’s state-level LIHTC program, for example, exempts LIHTC credits from the annual state cap if development takes place in counties affected by natural disasters.82 At the federal level, lifting the cap could unlock more LIHTC funding and construction.

Example 3: Innovate and refine tax abatements

In addition to LIHTC programs, “as of right” tax abatements could help affordable housing investors further spur development.

- In Illinois, the Affordable Housing Special Assessment Program offers property tax abatements for developers that make a minimum share of units affordable for families earning less than 60 percent of area median income (AMI) for at least ten years.83

- In Florida, up to 100 percent of units in multifamily developments are exempt from property tax if a minimum share of units is affordable to households earning less than 80 percent of AMI.84

These programs can help make affordable housing more attractive for investors, and further innovations could be explored. For instance, philanthropic capital could help make these abatements more accessible by filling gaps in predevelopment financing for smaller developers that may lack the up-front capital and expertise needed to pursue these programs.85 Furthermore, philanthropic or mission-driven capital could provide forms of guarantees to reduce the regulatory risk of these state-run programs. Other states and jurisdictions could also consider launching similar programs to spur housing investment.

Example 4: Unlock more capital for multifamily affordable housing

The Community Reinvestment Act (CRA) encourages financial institutions to invest in affordable housing and other development projects, which enabled $227 billion in mortgages and small-business loans and $151 billion in community development loans to flow to low- and middle-income communities in 2022.86 CRA-compliant loan portfolios could enhance affordable-housing developers’ access to financing.

- More preassembled portfolios of CRA-compliant multifamily housing investments could reduce time and complexity to assess investments and help banks, particularly smaller institutions, overcome potential capacity constraints that may impede investments in affordable housing.

- Community Capital Management, a registered investment adviser, manages $6.3 billion in CRA-qualified investments. It has invested $130 million in mortgage-backed securities for low-income housing through its Affordable Housing ETF since September 2024.87

- CRA-compliant loan portfolios could also expand the secondary loan market for CDFIs. Between 2018 and 2022, CDFI lending more than doubled, reaching $67 billion in originations and $14 billion in loan sales.88 However, limited secondary loan markets prevent CDFIs from replenishing capital to originate new loans. More than half of CDFIs that report higher demand also report being unable to meet that demand.89 Creating portfolios of CRA-compliant CDFI loans could help CDFIs meet this demand with a larger secondary loan market,90 particularly since changes to the CRA expected to take effect in 2026 will make purchasing CRA-eligible loans from CDFIs simpler and more beneficial for banks.91 Scale Link is one nonprofit fund that pools CDFI loan packages to sell to banks. Scale Link has purchased 3,500 loans from CDFIs, sold nearly $37 million to bank partners, and provided $55 million in capital to CDFIs since late 2020.92

More solutions like these may help a greater share of institutions make affordable housing investments.

Impact of scaling these strategies

If the PAB cap for LIHTC were lifted and states that have maximized their PAB allocation increased PAB issuance each year by 14 percent to 16 percent,93 we estimate that an additional 330,000 to 380,000 LIHTC units could be constructed, affecting 70,000 to 85,000 Black households over ten years. This estimate assumes an additional $24 billion to $34 billion in annual PAB allocation by the federal government for ten years, which represents nearly double the total multifamily PAB allocation in 2020 ($17.2 billion).94

If financing strategies expanded the secondary loan market for CDFIs such that CDFIs were able to increase multifamily housing lending by approximately $1.5 billion to $2.0 billion each year, we estimate that the United States could finance approximately 40,000 to 60,000 additional multifamily units, making an impact on 9,000 to 13,000 Black families over ten years.95

Theme 3: Scale off-site home construction

The problem today

Traditional, on-site construction is time-consuming and expensive. Producing components in factories and assembling them on-site could help address high material prices and skilled-labor shortages96 and offer the kind of productivity and innovation that has helped other sectors of the economy.

Despite significant cost savings, prefabricated techniques—particularly modular construction97—have struggled to scale. Modular construction (Exhibit 12) is 20 percent to 50 percent faster, 20 percent cheaper,98 and more energy efficient99 than traditional methods. Yet it represented only 3 percent of multifamily and 4 percent of single-family completions from 2000 to 2023.100 This section of the report explores examples of ways to scale home construction.

Example 1: Standardize state and local codes

Federal HUD codes apply to manufactured but not modular housing, which is governed by state and local codes.101 As a result, states generally do not certify construction from an out-of-state factory without detailed inspections. Standardized codes could enable modular construction companies to operate in multiple states efficiently, as in the following examples:

- In Hawaii, the Federal Emergency Management Agency (FEMA) used modular homes constructed out of state to replace 2,000 homes destroyed by the Maui wildfires of August 2023.102 To do so, FEMA relied on a set of off-site construction standards developed by the Modular Building Institute (MBI) and the International Code Council.

- Colorado, Montana, Rhode Island, Utah, and Virginia leveraged MBI’s proposed industry-wide guidelines.

Example 2: Develop tailored financing and lender education on the benefits of modular construction

Modular construction is considered riskier than standard construction because of its relative novelty and the highly customized nature of units, and therefore can require more up-front capital than traditional construction. A study by the National Renewable Energy Laboratory found that developers can require up to 30 percent higher equity for modular versus on-site construction.103

- Tailored financing methods—in which a portion of funds is paid when materials are delivered rather than when construction is completed and inspected—may reduce financial barriers. These methods have seen some success with lenders,104 particularly when modular builders can educate investors about the benefits of off-site construction.105 According to HUD, “a lack of education, knowledge, and awareness” is a primary factor in the difficulty of financing for off-site manufacturing facilities and individual projects.106

- Greystar Real Estate Partners, the country’s largest apartment operator, recently opened its first modular apartment complex in Pennsylvania.107 Greystar also explained the capital structure for modular projects to lenders and took them on factory tours.

Example 3: Explore long-term partnerships between construction companies and the public sector

Long-term partnerships between the public sector and off-site construction companies may address barriers to financing and scalability. Government agencies have greater flexibility on financing terms. For example, Volumetric Building Companies—a vertically integrated manufacturing and construction group focused on modular multifamily housing—has received funding from the Pennsylvania Housing Finance Agency and the LIHTC program to build 32 modular rental units in West Philadelphia.108 Other jurisdictions could explore similar partnerships to scale off-site production.

While this section of our report primarily focuses on modular multifamily construction, modular and other off-site building methods are also important in single-family construction. Today, manufactured single-family homes (traditionally known as “mobile homes”) offer a more affordable entry point to homeownership, particularly in rural areas.109 Allowing homeowners to title manufactured homes as property, relaxing mandates such as permanent chassis requirements (which can be used to exclude manufactured homes from most residential zones),110 and helping mobile-home residents organize to buy the land they live on may make ownership of manufactured homes more affordable and accessible.

Impact of scaling these strategies

Implementing these strategies to streamline codes and enhance lender education could add 120,000 to 190,000 affordable multifamily modular units over the next decade, with 27,000 to 43,000 units for Black households.111 This does not include the impact of scaling other types of off-site construction or applying the strategies to single-family construction, which could further increase the impact of this solution.

Theme 4: Reinvest in public housing and shared-equity models

The problem today

Public housing—which faces a $115 billion backlog in capital to address basic quality, safety, and health problems—has suffered from decades of underinvestment in both physical units and neighborhoods. However, public housing remains fundamental to affordability for more than 900,000 low-income families,112 nearly half of whom are Black.113

Moreover, there are more than 300 shared-equity entities across the United States that provide critical solutions for housing affordability and wealth accumulation, with several innovations emerging.114 We examine strategies to reinvest in existing public housing and further explore shared-equity ownership models.

Example 1: Expand PHA capacity for RAD conversions

The Rental Assistance Demonstration (RAD)115 gives public housing authorities (PHAs) the financial means to preserve and improve public housing while addressing the nationwide backlog of deferred maintenance.116

- Under RAD, PHAs can leverage public and private debt and equity to convert up to 455,000 Section 9 public housing units to Section 8 project-based units with a permanent affordability contract.

- However, PHAs often lack the technical capacity to facilitate RAD conversions, especially when rehabilitation costs are high. In a standard RAD conversion, a PHA reallocates its annual operating and capital subsidies into a Section 8 rent subsidy.117 Ensuring that projected rental income covers costs is an essential, but time-intensive, exercise. Better access to technical assistance and sophisticated financial tools could help PHAs improve project viability, risk management, and financial oversight.

- Expanding PHA capacity for RAD conversions has demonstrated the potential for impact, but not without some mixed results.118 PHAs could also benefit from more robust internal capabilities for assessing project equity and navigating LIHTC applications. Investors may be reluctant to back projects that require major rehabilitation if they lack visibility into expected returns and tax exemptions.119 HUD notes in its RAD conversion guide that PHAs with recent success in projects involving multiple financing sources “may likely have internal capacity to successfully plan and carry out a RAD conversion.”120 However, for PHAs that lack this experience, support for engaging external development partners and building out their teams could be critical.

Example 2: Scale public–philanthropic capital for shared-equity housing solutions

One common shared-equity model is community land trusts (CLTs). In traditional CLT models, CLTs purchase land and manage holdings either by selling structures to buyers who agree to certain terms at resale or by renting to low-income families at submarket rates.

- First Homes CLT sells homes at below-market prices to homebuyers who earn less than 80 percent of AMI and buys them back on resale to maintain income covenants for qualified buyers. Founded with a $4 million initial grant, First Homes helped alleviate an affordable housing shortage for Mayo Clinic’s 28,000 service workers in the Rochester, Minnesota, area.121

- An alternative model is for CLTs to manage income-protected units within market-rate developments. The nonprofit Chicago Housing Trust works with the city to preserve long-term affordability for homes created through inclusionary zoning and other city-led programs. Like other CLTs, Chicago Housing Trust aims to level the playing field for first-time buyers by selling price-restricted homes, but unlike some other CLTs, it also maintains affordable rental units on behalf of the city.122 Scaling the impact of similar housing trusts would likely require additional support from philanthropic capital, which can provide funding for land acquisition, technical assistance, and down payment assistance to first-time buyers purchasing shared-equity homes. Given that 55 percent of CLTs’ net income comes from donations, one way to scale CLTs is to increase the philanthropic capital available to them.123

- Moreover, innovations such as mixed-income-housing trusts124 and impact-centered renter-equity models (for example, Enterprise Community Partners’ Renter Wealth Creation Fund125 and Up&Up126) have also shown early promise and are additional models for continued exploration.

Impact of scaling these strategies

If the RAD program expands as required to reach the conversion cap, 110,000 to 200,000 units127 could be converted over the next decade, with Black households gaining access to an additional 48,000 to 85,000 units.128

Theme 5: Revamp housing choice vouchers

The problem today

Housing choice vouchers reduce homelessness,129 alleviate poverty,130 and facilitate moves to better neighborhoods.131 The nation’s largest source of rental assistance, Section 8 housing choice vouchers serve more than five million people in 2.3 million households.132 Forty-five percent of voucher recipients are Black.133

However, only one in four eligible families receives vouchers or other rental assistance, and the average wait time is two and a half years.134 And only 60 percent of families that do receive assistance find a housing unit to apply it to, while the rest must forfeit the support.135 Lease-up rates are even lower for Black residents.136

Example 1: Scale pilot experiments that provide direct rental assistance to families

Administrative burdens—lengthy inspection processes, occasional rent negotiations with PHAs, and potentially delayed rental payments—could make landlords reluctant to rent to voucher holders. Pilot programs in Philadelphia, Southern California, and Washington, DC, have experimented with rental assistance paid directly to families to alleviate these burdens.

- Early randomized evaluation evidence from Washington, DC, where the city council used $5 million in local funds to provide $7,200 in annual rental assistance to 125 families for four years, suggests that flexible assistance reduces the use of other homelessness services.137 These other services—emergency shelter, short-term homelessness prevention, and rapid rehousing—tend to cost more than direct rental assistance.

- A national trial comparing direct rental assistance to traditional vouchers could explore other outcomes such as lease-up rates, housing, and neighborhood quality with the rigor of a larger sample size. HUD has indicated that it may consider such a trial.138

Example 2: Improve landlord collaboration

Up-front guarantees for landlords and streamlined rental processes such as inspection or payments could help remedy administrative burdens. While HUD’s Moving to Work study assesses the impact of giving landlords incentives to rent to voucher holders (with results expected in 2026), locally led landlord partnerships may contribute to more efficient voucher programs.139

- Virginia Beach’s Landlord Engagement and Partnership initiative offers landlords predictable payment schedules, automatic direct deposits, up-front security payments, dedicated customer service staff to address landlord questions, and case managers to support tenants.140

- Albuquerque’s Landlord Engagement Program offers up to $3,000 worth of repairs, $1,000 to help meet inspection standards, $500 for application and past-due fees, and funding for prolonged vacancy if repairs are needed from a previous tenant.141 This additional layer of security is particularly important for mom-and-pop landlords in a city where 85 percent of rentals are independently owned.142

- These strategies could work in tandem with increased monitoring and enforcement of protections against source of income discrimination. HUD’s Source of Income Protections website, launched in March 2024,143 may be an example of a step in the right direction.

Example 3: Increase access to high-opportunity neighborhoods

Expanding access to high-opportunity neighborhoods has the potential to significantly improve long-term outcomes for low-income families.144 Additional voucher-related approaches would enable families to “lease up” in high-opportunity neighborhoods that improve outcomes for children.

- One strategy is for PHAs to adopt small area fair market rent (SAFMR) standards. Unlike traditional metropolitan-wide standards, SAFMRs set rent thresholds specific to individual zip codes. These standards may allow voucher holders to move into neighborhoods with lower crime, poverty, and unemployment.145 In 2023, 45 percent of households receiving vouchers used them in SAFMR areas.146 HUD already requires that PHAs in 65 metro areas use SAFMR, but those in non-designated areas may also opt in.147

- A second strategy is to scale counseling. In Seattle and King County, Washington, families who worked with a trained “housing navigator” to identify voucher-eligible units, submit rental applications, and access financial assistance were more than three times as likely to move to a high-opportunity neighborhood as those who received no assistance.148

Impact of scaling these strategies

If flexible rental payments, incentives for landlords, and housing counseling were scaled such that 75 to 80 percent of families offered vouchers were able to lease up by 2035 (compared with 60 percent for all families and 54 percent for Black families today149), approximately 220,000 to 290,000 additional families, including 150,000 to 190,000 Black families,150 would be able to use housing choice vouchers over ten years.

Maximizing national and local impacts

No single solution would fully address the affordable housing crisis or remedy barriers faced by Black renters and homeowners. However, the solutions outlined across the five themes we examined (Exhibit 13) would begin to tackle the gap by supporting an estimated 1.8 million to 2.3 million households over the next ten years.151 This would have a particular impact on Black households, who could occupy nearly 30 percent of the total affected housing units. While this would be a start at reversing the trend, more actions would be required to fully resolve the supply shortage.

These solutions should and must be tailored to meet the needs of local communities (Exhibit 14). Using the community profiles introduced earlier, we identify where these solutions are likely more relevant at the community profile level (recognizing the need for hyperlocal geographic context to fully vet and assess the potential of these solutions for any specific geography).

Our analysis is not exhaustive of the full range of affordable housing solutions. Additional context on our methodology and assumptions is provided in the appendix, section 3. For a more expansive list of potential affordable housing ideas,152 please see the appendix, section 2.

Conclusion: Acting on opportunities

Addressing the issues outlined in this report could significantly improve the housing supply in the United States, which in turn would enhance the quality of life, employment opportunities, educational attainment, and financial well-being of American families, with a particularly positive impact on Black families.

A broad cross-section of stakeholders can play a role in resolving this crisis—from individuals and institutions across federal, state, and local governments to developers, investors, and nonprofits—and help put more American families on a path to greater economic opportunity.

This report is by no means comprehensive but offers the start of a new way forward. Imaginative solutions across sectors are critical for addressing this crisis, and we look forward to new ideas and innovations that can help deliver benefits for American families.

Related Articles

The state of Black residents: The relevance of place to racial equity and outcomes